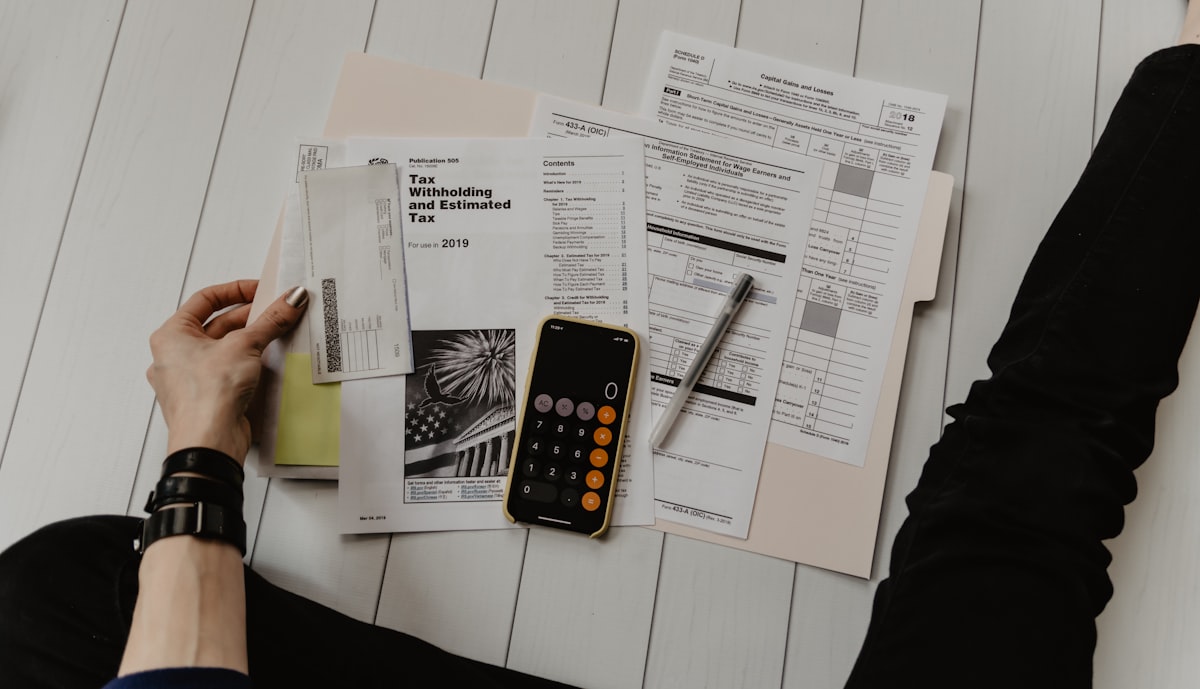

Why Budgeting Matters More Than Ever in 2026

As global inflation stabilizes and interest rates shift across major economies, personal financial planning has become a critical skill. In 2026, building wealth requires more than simply earning more — it demands intentional budgeting strategies that align with modern financial realities.

Whether you are a young professional starting your career or a seasoned investor looking to optimize cash flow, smart budgeting lays the foundation for long-term financial freedom.

The 50/30/20 Rule Reimagined for 2026

The classic 50/30/20 budgeting framework — allocating 50% of income to needs, 30% to wants, and 20% to savings — remains a powerful starting point. However, financial experts now recommend adjusting these ratios based on individual circumstances.

With rising subscription costs and digital spending habits, many advisors suggest a modified 40/30/30 approach, where 30% goes directly toward savings and investments. This shift reflects the growing importance of building emergency funds and retirement portfolios early.

Automate Your Savings and Investments

One of the most effective budgeting strategies in 2026 is automation. Setting up automatic transfers to savings accounts, investment portfolios, and retirement funds eliminates the temptation to overspend.

Modern fintech apps like Acorns, YNAB (You Need A Budget), and Revolut make it easier than ever to automate round-ups, schedule investments, and track spending patterns in real time. Automation turns disciplined saving from a daily struggle into a seamless habit.

Track Every Dollar with Zero-Based Budgeting

Zero-based budgeting assigns every dollar of income a specific purpose before the month begins. Unlike traditional budgeting, where leftover money often disappears into unplanned purchases, this method ensures complete financial accountability.

Tools like EveryDollar and Mint allow users to create zero-based budgets digitally, making it simple to categorize expenses and identify areas where spending can be reduced.

Cut Hidden Expenses That Drain Your Wealth

Small recurring expenses often go unnoticed but can significantly impact long-term wealth. Common hidden costs include:

- Unused subscriptions — streaming services, gym memberships, and software trials

- Bank fees — maintenance charges, ATM fees, and foreign transaction costs

- Impulse purchases — online shopping driven by targeted advertising

- Dining out frequently — meal planning can save hundreds monthly

Conducting a monthly expense audit helps identify and eliminate these financial leaks, redirecting funds toward wealth-building activities.

Build an Emergency Fund Before Investing Aggressively

Financial planners consistently recommend maintaining three to six months of living expenses in a liquid emergency fund. In 2026, high-yield savings accounts offer competitive interest rates, making emergency funds work harder while remaining accessible.

Without an adequate safety net, unexpected expenses like medical bills or job loss can force individuals into high-interest debt, undermining years of careful budgeting.

Leverage High-Yield Savings and Money Market Accounts

Traditional savings accounts often fail to keep pace with inflation. In 2026, high-yield savings accounts and money market accounts offer significantly better returns, with some institutions providing annual percentage yields (APY) above 4.5%.

Parking emergency funds and short-term savings in these accounts ensures your money grows while remaining liquid and accessible for unexpected needs.

Invest Early and Consistently

The power of compound interest makes early and consistent investing one of the most reliable paths to wealth. Even modest monthly contributions to index funds or ETFs can grow substantially over decades.

For beginners, dollar-cost averaging — investing a fixed amount at regular intervals regardless of market conditions — reduces risk and eliminates the stress of trying to time the market.

Reduce Debt Strategically

High-interest debt, particularly credit card balances, is one of the biggest obstacles to building wealth. Two proven strategies for debt reduction include:

- The Avalanche Method — paying off the highest-interest debt first to minimize total interest paid

- The Snowball Method — paying off the smallest balances first for psychological momentum

Choosing the right approach depends on personal motivation style, but both methods accelerate the path to becoming debt-free.

Set Clear Financial Goals with Timelines

Budgeting without clear goals lacks direction. Setting specific, measurable financial targets — such as saving $10,000 for an emergency fund within 12 months or paying off $5,000 in credit card debt by mid-year — creates accountability and motivation.

Breaking large goals into monthly milestones makes them achievable and helps maintain momentum throughout the year.

Final Thoughts: Start Today, Build Tomorrow

Wealth building in 2026 is not about earning a six-figure salary — it is about managing what you earn with intention and discipline. By adopting smart budgeting strategies, automating savings, cutting hidden expenses, and investing consistently, anyone can take meaningful steps toward financial independence.

The best time to start budgeting was yesterday. The second best time is right now.